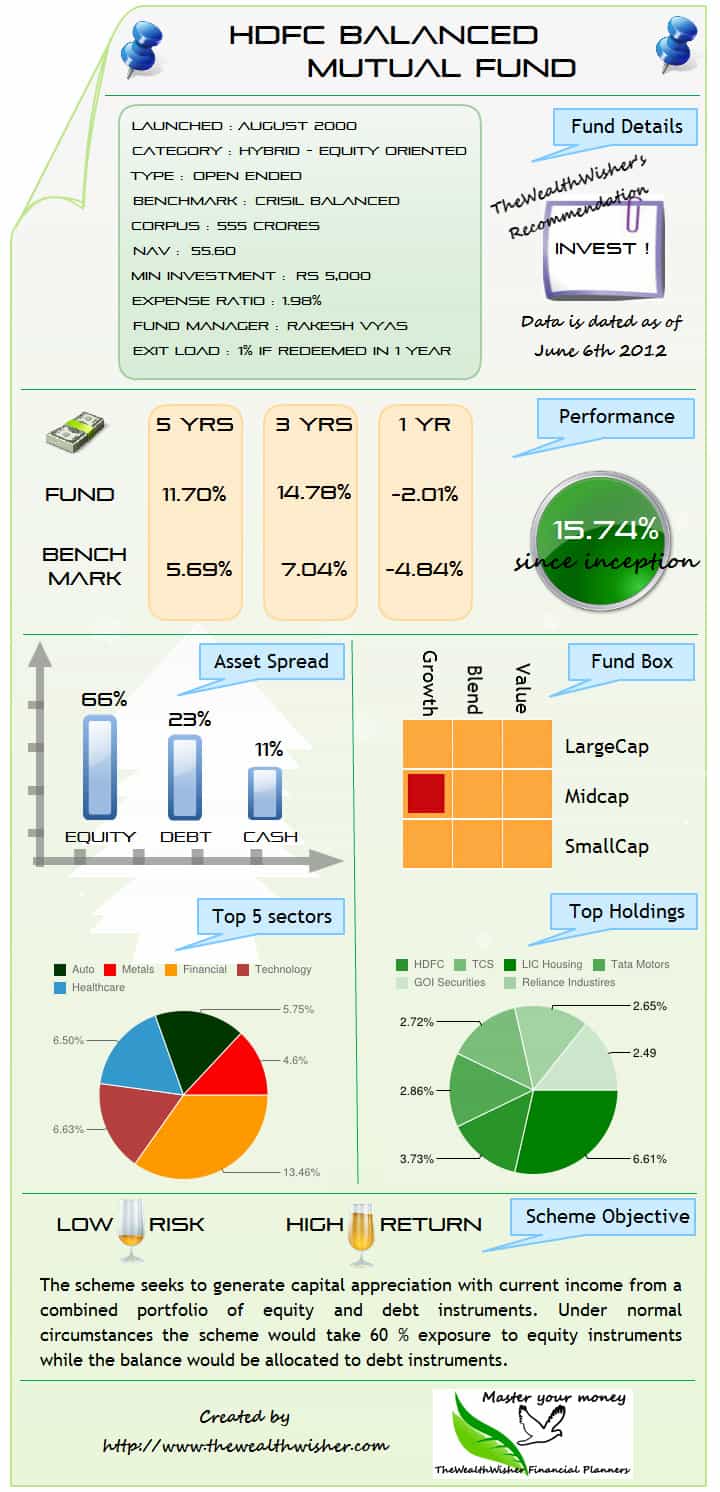

OK, HDFC Balanced Mutual Fund needs no introduction. But I guess it will be a shame if we don’t cover this here.

This is a hybrid fund with around 15% returns over the last 12 years, as of writing. With around 20% in debt and 10% in cash and the rest in equity, HDFC Balanced fund does indeed provide great returns via a balanced approach.

While you run through this, please provide your thoughts on other mutual funds in the same category which you think are better and which you might hold. I receive many queries on HDFC Balanced versus HDFC Prudence and I will not be surprised if someone asks that in the comments section.

Click on the image to see a clearer, better and bigger graphic.

{kind=link}

Excellent analysis. HDFC Balanced has been one of the consistent performers, 15% returns since inceptions speaks for itself.

Indeed, it is one of the best ones around.

Nice concept, but at some places fonts are not clearly readable. Colours used at some places, are also little jerky. I think you need to do some rework on the overall layout part. These were just my honest feedback and I may be wrong. 🙂

I did have a relook and I thought that if you check the biggest size of the infographic, all fonts are visible. Let me know which one you are referring to specifically.

I think Sandip is referring to the picture in the article itself because it is a little hazy for me too. However, when I open the picture in a separate window it looks perfectly alright.

How does it compare with SBI dynamic?

@Dip,

Are you referring to SBI Dynamic Bond fund, if yes then its a Debt fund and we cannot compare both of these. Moreover it returns over the last 5 years is just 5%. It does not invest in equity whereas HDFC Balanced has around 20% investment in equity.

Exactly, thanks for the advice Rakesh.

I really like this fund. I have SIP in HDFC balanced fund, it’s part of my medium term savings.

Good thing is most of the times you won’t see negative returns for your investments (for SIPs), even if the market is down. People who are new to MF investment can start SIPs with this fund for few months and understand/learn how SIP works, later they can build their portfolio.

One of my top favourites in Balanced Fund categories. However, as a rule, I tend to avoid recommending any of my resident indian clients to invest into Balanced Funds. There are much better options such as PPF, PF where Resident Indians can invest to have a debt component in their portfolio which are tax efficient as well.

Balanced Funds are best poised to tackle the debt component for NRIs – considering that they cannot invest into PPF.

Whats your opinion this ?

@BFA,

Rightly said but then you don’t advise your clients to invest in Real Estate in their country of residence. For eg. Real Estate prices have fallen about 50-70% in some areas, moreover you could get a good house much cheaper in US now then many other cities in our country.

I know couple of NRI’s based out in US investing heavily in real estate.

@BFA

PPF, PF looks good for retirement portfolio. Wouldn’t it be good to invest in Balanced fund for other goals, without much efforts to invest in diff equity and debt MFs and tracking debt/equity ratio + You can’t always redeem PPF, PF when you want money in 3-10 yrs period.

I agree with you Chirag, I think balanced MFs are great products giving a perfect balance as the name suggests. Instead of running behind and tracking different equity and debt MFs, one can always opt for balanced funds. These are great for newbies in the field as well.

You still need to track balanced MFs, you cannot skip it, can you ?

I seldom advise products that are a mix of equity and debt because you can achieve them with pure products also as you rightly say. But I guess for laid back investors such products are good as the person gets an exposure to to both asset classes.

NRI’s can invest on other debt products as well apart from balanced funds I guess which will help them with the debt exposure.

Ain’t Balanced funds are good for people with less risk appetite?

They are good but not the only avenue. You can either skip them or have them, I chose the former.

Are you saying investment in PPF is better than balanced MFs in long run? That’s interesting! Is there any stats you can share to support this fact?

@ Vivek – Definitely PPF would be better than balanced funds’s debt component after fund management charges. Do not forget, balanced funds are Equity + Debt, whereby minimum 65% is Equity. However, that doesn’t prevent the fund manager to go upto 80% on Equity. Hence you may be living in a false comfort that you have a good debt buffer via Balanced Funds.

For NRIs, it changes the picture. They don’t have many tax friendly debt options, hence balanced funds are excellent for them. They can’t invest into PPF. NRE FDs, though tax free in India, are taxable in their foreign countries (except Middle East) as their normal tax slabs, often attracting over 30% tax. Hence Balanced Funds are much better suited for them considering that they don’t have to pay tax till the time they don’t sell them and it would considered as Capital Gain which is generally taxed at lower limits.

However, again if I have to go for the debt component in their portfolio, I might even bring in Monthly Income Plans in their portfolio which gives me a comfort that atleast there would be over 75% debt. A setback is Tax aspect in India though !

Excellent response BFA.

This infographic is very good, gives one pager summary about a MF. I think you should continue publishing for other popular MFs as well.

One question I always keep hearing, which one is better between the two: HDFC Balanced or HDFC Prudence? Can we have a comparison infographic on the two? or may be some discussion by other readers here?

@Vivek,

I don’t think we can compare Prudence with Balanced, Prudence is more of an hybrid fund. Prudence invests about 70% in equity where Balanced invests about 20% in equity. So results would wary…..

Well as per the above infographic HDFC balanced is investing 66% in equity. So, I guess they can be compared?

Will do sir !

Hi TheWealthWisher,

It’d be great if you can come up with your analysis on the new NFO that ICICI is putting up : ICICI Prudential US Bluechip equity fund. I am interested in knowing the currency hiccups and whether it’s really a worthwhile investment.

I have a small amount left that can be invested in a mutual fund and I am not yet decided on any. Currently, I have ICICI Pru Focused Blue Chip, HDFC Growth and IDFC Premier Equity and trying to check if I should go with a Large Cap or Large/Mid cap.

Thanks

Rohit

Just done that but I read your comment after ding the post. Note that this is a NFO that offers investment in US equities primarily. You seem to have good funds in your kitty already.

@Rohit,

What is your rational to invest in NFO’s? Instead why don’t you increase SIP’s in your current MF. IDFC Premier Eq. is been a consistent performer. HDFC Growth has been and under-performer from sometime, why don’t you look at HDFC Top 200 / HDFC Equity.

Hmmmm. I thought I’d see if there’s any good in an NFO. So it’s better to stick with consistent MF’s rather than trying to go to risk an NFO ?

@Rohit,

Yes, that’s right stick to your consistent performing Mutual funds.

@Rohit, One of the criteria to invest in MFs is to check its past performance.

How a MF has performed during the ups and downs of the market?

How a MF has performed as compared to other funds in the same category?

So, based on above investing in NFOs is not a great idea. People tend to invest in NFOs just because of the general misconception that the initial offer is always cheap and the price will only go upwards from here.

I would agree with Vivek on this.